Key Takeaways: Carry Transparency and Employee Retention

- Most employees with carry allocations can't answer basic questions about their own position: what's vested, what it's worth, what has to happen before they see a dollar, and what they'd lose if they left tomorrow.

- That opacity isn't intentional. It's the byproduct of carry data living in finance-team spreadsheets that were never designed to be shared or accessed by a broader audience.

- When carry is opaque, its value as a retention tool degrades. Employees discount what they can't see, and every unanswered question becomes an ad-hoc request on the CFO's desk.

- A total compensation dashboard that shows carry alongside co-invest, salary, and bonus turns carry from an abstract line item into a tangible reason to stay.

You granted your team carry for a reason. It's the most meaningful long-term incentive your firm can offer, a direct stake in the economics you're building together. For founding partners, carry is the core of the business model. For the growing bench of principals, VPs, and operating partners who now participate, it's supposed to keep them invested in the firm's success over a ten-year fund cycle.

Here's the problem: most of them have no idea what they actually hold.

They received an award letter when they joined. They probably read it. They may remember the headline number: "You'll receive X% carry in Fund III." Beyond that, the details are murky. What's vested? What's it worth? What has to happen before they see a distribution? What do they forfeit if they leave?

These are the questions every rational employee with a carry grant thinks about, silently, constantly, and with increasing urgency as they approach career decision points. But most won't ask, because they worry it makes them look greedy or disloyal. So the questions go unasked, the uncertainty compounds, and the retention value of carry quietly erodes.

The Carry Questions Your Team Won't Ask Out Loud

Every carry holder is thinking about some version of these questions. They just express them differently depending on seniority and comfort level.

1. "What's actually vested?"

The most fundamental question, and remarkably few participants can answer it. They know they have carry. They may know their percentage. But the vesting schedule, set three years ago in a document they've filed away, isn't something they track.

When the answer requires digging out the award letter and doing mental math against a start date, most people don't bother. The carry sits in a mental category labeled "probably worth something, eventually," which is not the engagement signal your firm intended.

2. "What's it worth right now?"

Even participants who know their allocation and vesting status rarely know the estimated dollar value. Getting there requires mapping their allocation against the fund's current NAV, applying waterfall mechanics, and distinguishing between vested and unvested value. Most employees can't do that calculation, and most firms don't provide it.

Firms spend enormous effort on fund valuations: quarterly NAV updates, portfolio reviews, investor reporting. But that data almost never flows down to the individual carry holder.

The fund's performance gets reported to LPs in meticulous detail. The employee who holds 2% of the carry pool gets a number they made up.

3. "What has to happen for me to see a dollar?"

This separates theoretical compensation from tangible compensation. Carry sounds valuable in an offer letter, but for most employees it stays abstract until they understand the chain of events:

- Investments need to exit

- The fund needs to return capital and clear its hurdle

- The GP's carry share gets calculated

- Their individual allocation, at their current vesting percentage, determines their share

That chain is straightforward to anyone who's operated a fund. It's genuinely opaque to a principal from consulting, an operating partner from industry, or a VP two years into their first PE role. When the answer is "your carry depends on exits that may not happen for five more years," the motivational power of the grant depends entirely on whether the employee trusts the numbers and understands the path.

4. "What happens if I leave?"

The question with the highest emotional stakes and the lowest transparency. Every carry holder has thought about it, not because they're planning to leave, but because understanding the downside is how people evaluate any financial position.

The answer lives in forfeiture provisions that vary enormously across firms:

- "Good leaver" vs. "bad leaver" definitions

- What happens to unvested carry

- Whether vested carry is retained or subject to conditions

- How departure timing affects the outcome

Few employees understand these terms in detail. The resulting dynamic is that people stay partly because of carry they believe they'd lose, without knowing exactly what they'd lose. That's ambiguity functioning as a handcuff, and it breaks the moment a recruiter shows up with a concrete offer.

5. "How does carry fit with everything else I earn?"

Carry doesn't exist in a vacuum. Employees also have base salary, bonus, co-invest returns, GP commit obligations, and benefits. The total picture is what determines how they evaluate their position relative to alternatives, and almost no firm presents it in an integrated way.

Instead, carry information comes from one source (if at all), bonus data from HR, co-invest statements from fund ops, and K-1s from tax. Assembling these into a coherent total compensation view falls to the employee, who typically can't do it because the data doesn't exist in a format that allows it.

6. "Am I being treated fairly?"

Nobody will ever ask this directly, but it underlies all the others. When carry is opaque, employees fill the vacuum with assumptions, comparisons, and speculation. They talk to peers at other firms. They compare notes with colleagues. They form beliefs about their position that may or may not be accurate, and they make career decisions based on those beliefs.

Transparency here doesn't mean disclosing everyone's allocations. It means giving each participant enough visibility into their own position that they don't need to guess.

Why Most Firms Don't Provide This Transparency

For most firms, the opacity is an operational constraint, not a deliberate strategy.

Carry data lives in finance-team spreadsheets built for internal tracking, not participant communication. Producing an individual statement means pulling data from fund-level models, calculating vested and unvested positions, estimating value, and formatting it all into something presentable. That's an hour per person. For forty carry holders, it's a multi-day project every quarter.

Most finance teams don't have the bandwidth. They produce partner statements for the senior-most participants and handle everyone else ad-hoc. The VP who asks gets an answer. The principal who doesn't ask gets nothing. And the firm's carry program loses retention power across exactly the population most at risk of being recruited away.

The other barrier is sensitivity. Firms worry that showing unrealized estimates creates expectations that may not materialize. What if performance declines? What if employees fixate on the number? These are legitimate concerns, but complete opacity trades one risk for another: carry becoming valueless as a retention tool because nobody understands what they hold.

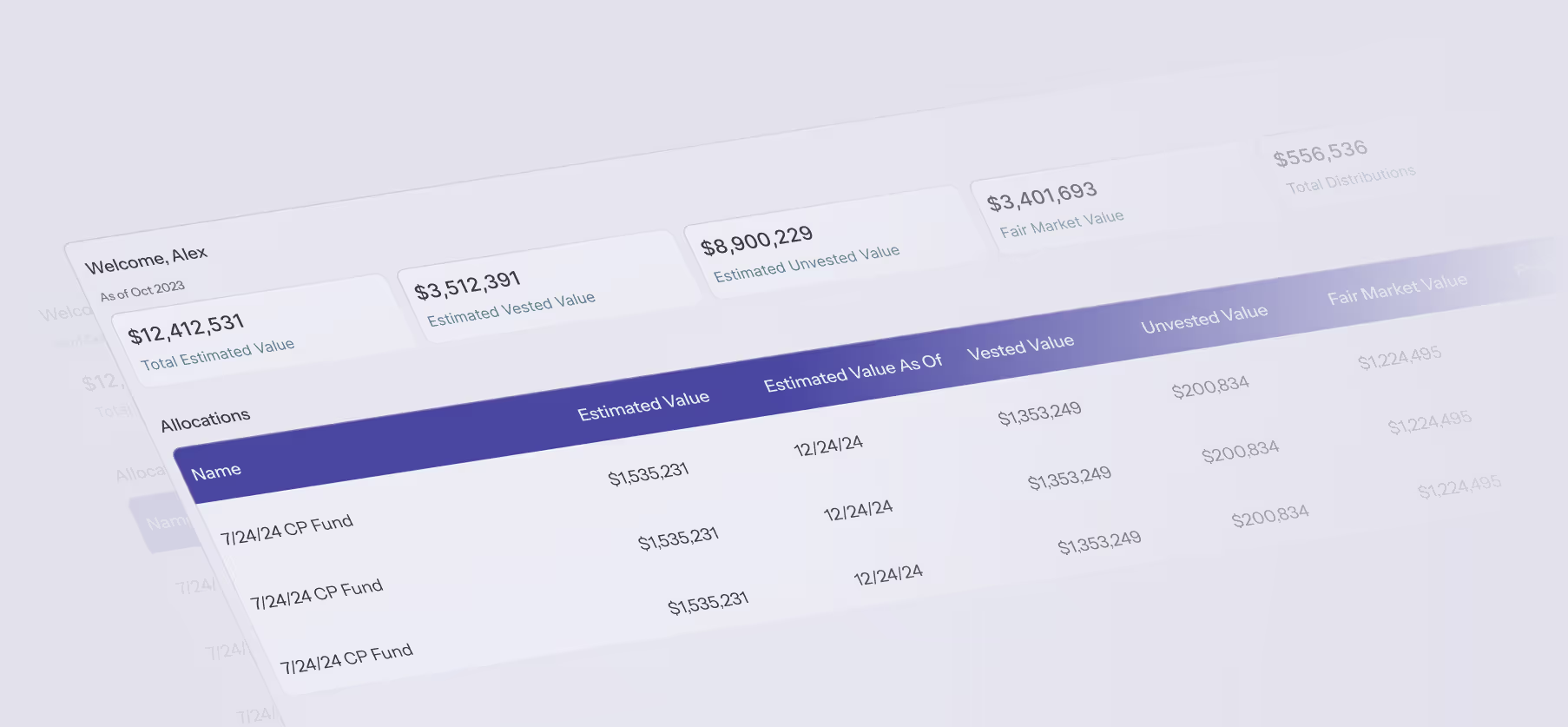

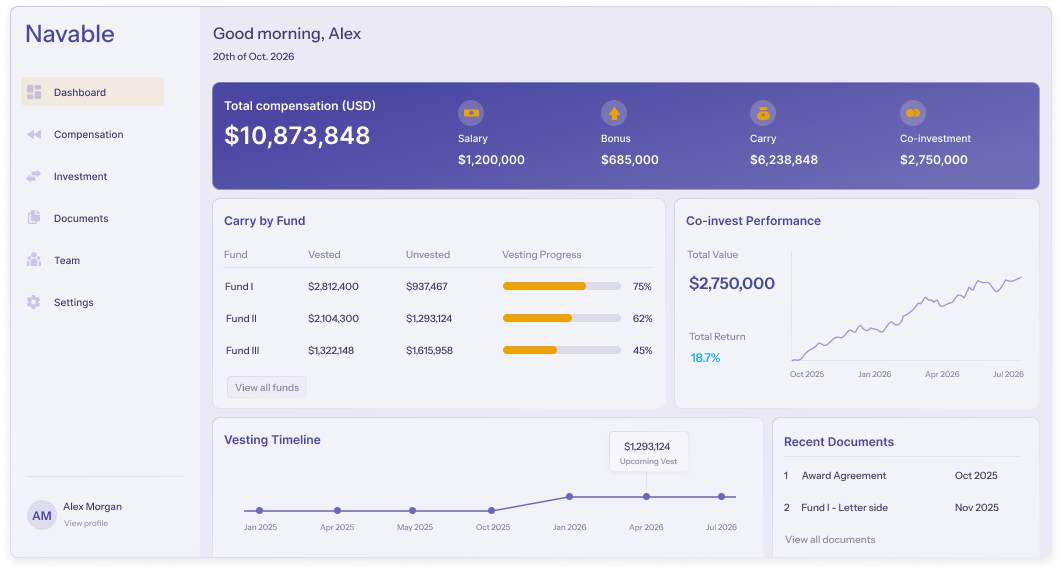

What a Total Compensation Dashboard Changes

The answer isn't better spreadsheets or more frequent ad-hoc statements. It's a participant-facing portal with a real-time, self-serve view of each person's complete compensation position.

A well-designed dashboard shows:

- Carry allocations by fund, with vesting status and schedule

- Estimated carry value (vested and unvested), updated each valuation cycle

- Co-invest commitments, capital called, and performance

- Base salary and bonus history

- GP commit obligations if applicable

- A consolidated total compensation view bringing everything together

The dashboard doesn't replace conversations with the CFO for senior partners. It eliminates the sixty other conversations that are really just data requests disguised as questions.

When a principal can log in and see $1.2M in vested carry value across two funds, 60% vested on a four-year schedule, with $180K in co-invest returns, they don't need to email the controller. They have their answer. They can see, concretely, what they'd walk away from.

That's what turns carry from an abstract promise into a tangible retention anchor.

The Business Case for Carry Transparency

The firms that provide real carry transparency do it because it works.

1. Reduced ad-hoc reporting burden.

Every question a participant answers through a portal is one that doesn't land on the finance team's desk. For firms with thirty or forty carry holders, the time savings are meaningful, especially around year-end.

2. Stronger retention signal.

An employee who sees $800K in unvested carry, updated quarterly and clearly presented, makes a different career calculation than one who vaguely recalls "some carry in Fund III."

3. Better hiring conversations.

Showing prospective hires exactly what total compensation looks like, including projected carry value, makes offers more compelling than competitors who describe carry in abstract terms.

4. Cleaner compensation reviews.

When leadership has a consolidated view of every participant's total compensation, year-end reviews and promotion discussions are grounded in complete data rather than partial information stitched together from multiple sources.

Designing Transparency That Works

Carry transparency doesn't mean radical openness. It means the right amount of visibility for each audience.

Role-based access is essential:

- Partners see allocations across all funds

- Employees see their own position only

- HR sees compensation-level views

- Finance sees everything

- One data source, different views based on role

Estimated values need context:

- Label unrealized estimates clearly, tied to the most recent fund valuation

- Present enough context that participants understand what drives the number

- Build trust through responsible transparency, not naivety

Consistency matters more than frequency:

- A quarterly update participants can rely on beats sporadic statements produced on request

- A steady cadence signals institutional commitment, not a one-off initiative

The Carry Conversation Your Firm Should Be Having

If your carry program is designed to retain your best people, ask yourself:

- Can those people actually see what they hold?

- Do they know what's vested?

- Do they understand what it might be worth?

- Can they see how it fits with the rest of their compensation?

If the answer to any of those is "not really," your carry program is working at a fraction of its potential. Not because the economics are wrong, but because the communication layer is missing.

The firms that get this right aren't the ones with the most generous carry plans. They're the ones where every participant can log in, see their position, and understand exactly what they have, what it's worth, and what has to happen for them to see a dollar.

That clarity is what turns compensation into alignment.

If your team can't see what they hold, Navable can help.

The platform gives every participant a real-time total compensation dashboard with carry, co-invest, salary, and bonus in one view. Book a demo →

FAQs: Carry Transparency and Total Compensation

Should employees see estimated carry values?

Yes, with appropriate context. Showing only allocation percentages without dollar values keeps carry abstract. Presenting estimated vested and unvested values, clearly labeled as estimates tied to current fund valuations, makes carry tangible and reinforces its retention effect.

What should a total compensation dashboard include?

At minimum: carry allocations by fund with vesting status, estimated carry value (vested and unvested), co-invest commitments and performance, base salary and bonus history, and a consolidated total view pulling from a single governed data source.

How often should carry information be updated for employees?

Quarterly, aligned with fund valuation updates. What matters most is consistency. Participants should know when to expect updates and trust that the data reflects the latest information.

Does carry transparency create retention risk if values decline?

Opacity is the greater risk. Employees who don't understand their carry make career decisions based on incomplete information. Employees who do understand it, even when values fluctuate, are better equipped to evaluate their total position rationally.

Can you provide carry transparency without a dedicated platform?

Through manually produced statements, yes. But at scale, the manual approach creates bottlenecks, inconsistencies, and staleness that undermine the transparency it's trying to provide. A self-serve portal is the only approach that scales.